Imagine the mortgage calculator as a seasoned cartographer, guiding you through the ever-shifting landscape of home loans. Just as a map helps you navigate unfamiliar terrain, a mortgage calculator steers you through the complexities of home ownership, revealing the financial path to your dream home.

Understanding Mortgage Calculators

At its core, a mortgage calculator is a tool for predicting your monthly mortgage payments. It does this by considering factors like the loan amount, interest rate, loan term, property taxes, and insurance. By inputting these figures, you can forecast your monthly expenses, factoring in everything from principal and interest to private mortgage insurance (PMI) and homeowner's association (HOA) fees.

One of the key features of advanced mortgage calculators is the ability to compare bi-weekly savings and refinance options. For example, if you pay your mortgage bi-weekly instead of monthly, you can significantly reduce the amount of interest you pay over the life of the loan. Additionally, these calculators can show you how much you could save by refinancing your existing mortgage to a lower interest rate.

How to Use a Mortgage Calculator Today

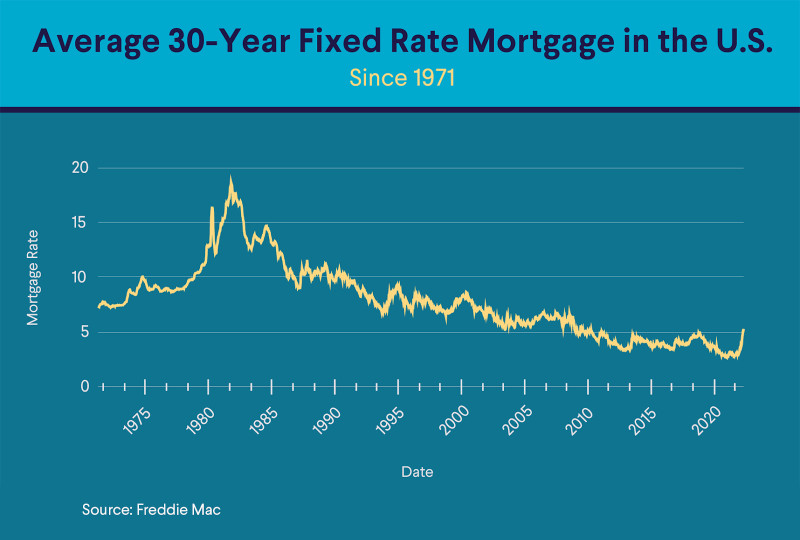

Today's mortgage rates are dynamic, fluctuating daily based on a variety of economic indicators. This makes a mortgage calculator an essential tool for prospective homeowners. The first step in using a mortgage calculator is to input your loan amount, which is the price of the home minus your down payment. For instance, if you're buying a $300,000 home with a 20% down payment, your loan amount would be $240,000.

Next, you'll need to determine your loan term, which is the length of time you have to repay the loan. This is typically 15 or 30 years, but other terms are available. Your interest rate is another crucial factor. This can vary based on your credit score, loan type, and current market conditions. Using a mortgage calculator, you can compare different loan terms and interest rates to see how they affect your monthly payments.

Why Current Mortgage Rates Matter

Mortgage rates are more than just numbers; they are the financial pulse of the housing market. When rates are low, as they have been in recent years, buying a home becomes more affordable, and the real estate market can boom. Conversely, when rates rise, as they have in recent months, the cost of borrowing increases, making homeownership more expensive and potentially cooling the market.

Understanding the current mortgage rates is essential for both buyers and sellers. For buyers, knowing the current mortgage rates helps them budget accurately and secure the best possible deal. For sellers, it provides insights into the market's health and the likelihood of finding a buyer. Whether you're a first-time homebuyer or looking to refinance an existing mortgage, staying informed about mortgage rates can save you thousands of dollars over the life of your loan.

“With spring homebuying season in full swing, aspiring buyers should remember to shop around for the best mortgage rate, as they can potentially save thousands of dollars by getting multiple quotes.” — Freddie Mac

The mortgage rates today represent a snapshot of the current economic climate. They are influenced by a myriad of factors, including inflation, unemployment rates, and Federal Reserve policies. For example, when the Federal Reserve raises interest rates, mortgage rates tend to follow suit, making borrowing more expensive. Conversely, when the economy is sluggish, the Fed may lower rates to stimulate growth, making borrowing cheaper and more accessible.

Remember, a mortgage calculator isn't just a tool for crunching numbers—it's a roadmap to financial stability. It allows you to visualize your financial future, helping you make informed decisions about one of the most significant investments of your life.